Is Lloyds at 97.5p the Hidden Stock Gem You Must Buy NOW—or Risk Massive Regret?

As stocks ebb and flow, opportunities can often arise unexpectedly for investors looking to buy into quality businesses at lower prices. This phenomenon has recently played out for Lloyds Banking Group (LSE:LLOY), a major player in the UK banking sector. After a remarkable rally of 34% over the past year, the stock has seen a notable decline of 14% in just four weeks as of March 6, prompting questions about its current valuation and future prospects.

The pullback in Lloyds' stock price may have been influenced in part by escalating tensions in the Middle East, events that the bank cannot control. Should these conflicts persist, investor sentiment could remain shaky. However, there are indications that Lloyds' valuation may have become overstretched, leading some shareholders to opt for profit-taking.

Typically, a stock's performance correlates with the publication of its financial results, and this is particularly relevant given that all five banks in the FTSE 100 have recently reported their earnings for 2025. This presents a timely opportunity for comparison of their current valuations.

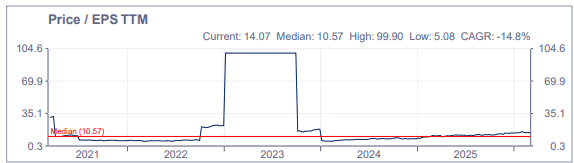

According to data from the London Stock Exchange Group, Lloyds currently holds a trailing twelve-month price-to-earnings (P/E) ratio that exceeds that of its peers. Over the past year, this ratio has been steadily on the rise, crossing above its five-year average (median) of 10.57. This increase raises questions about whether the stock's current price still reflects its true value.

The situation is similar with the bank's price-to-book ratio, where the recent stock price surge has created a larger disparity between its market valuation and the underlying net assets as reported on its balance sheet. In many cases, investors appear willing to overlook sizeable valuation multiples if growth continues unabated. A prime example of this is Rolls-Royce, which trades at nearly 45 times its anticipated earnings for 2025, largely due to consistent earnings upgrades that fuel its stock price momentum.

Looking ahead, analysts are optimistic that Lloyds' shares could soar past their 52-week high. Projections indicate that earnings per share may rise to 12.8p by 2028. If this figure holds true and is multiplied by its five-year average P/E ratio, the stock could be valued at 135p—marking a potential increase of 38% from its current price.

Moreover, predictions suggest dividends for 2026-2028 could reach 14.94p per share. This means an investment of £10,000 today could yield passive income of £1,532 over the next three years. However, as is often the case with dividends, there are no guarantees. If Lloyds' earnings come under sustained pressure, the bank may choose to cut its dividend to preserve cash.

Despite these optimistic forecasts, skepticism remains. The recent announcement by the Chancellor regarding the Office for Budget Responsibility's downgraded UK growth forecast for 2026 raises further concerns. As business confidence wavers and consumers feel financial pressure, an 83% increase in EPS by 2028, compared to 2025, seems overly ambitious, especially for a bank heavily reliant on domestic income.

In light of these factors, many analysts feel there are more compelling investment opportunities within the market. While Lloyds may present a tempting buy for some, the macroeconomic environment and the bank's reliance on domestic earnings could temper expectations moving forward.

As investors weigh their options, the fluctuating valuation of Lloyds Banking Group serves as a reminder of the complexities of stock market investing. The interplay of global events, economic indicators, and company performance will continue to shape the landscape for investors, making it crucial to remain informed and adaptable.

Oil Prices Surge, Market Plummets: Will You Lose Everything by Next Week?

You Won't Believe What Meta Just Revealed About Karnataka's Shocking Ban on Social Media for Kids!

Magic vs. Bucks: Can Orlando Pull Off a Shocking 4th Win Against the NBA Giants?

Korea’s Bold Move: Will This Shocking Public-Private Partnership Save Startups or Doom Them?

Colombia’s Epic Congress Battle: Who Will Claim Power as Shocking Candidates Emerge?

Messi’s Stunning Playoff Surprise: You Won't Believe What He Did Against D.C. United!

You might also like: