Bitcoin Conquers Wall Street, But This Shocking Twist Could Cost Investors Millions!

Bitcoin's recent integration with Wall Street was expected to usher in a new era of stability for the cryptocurrency. Instead, it has created a different kind of vulnerability—an over-reliance on American capital that is currently dwindling. Since October 10, approximately $8.5 billion has exited U.S.-listed spot Bitcoin exchange-traded funds (ETFs). Simultaneously, exposure to Bitcoin futures on the Chicago Mercantile Exchange (CME) has plummeted by nearly two-thirds from its late-2024 peak, now standing at around $8 billion. Prices on Coinbase, the platform favored by many institutional investors, have consistently traded at a discount compared to the offshore exchange Binance—indicating sustained selling pressure in the U.S. Consequently, Bitcoin’s value has dropped by more than 40%, even as stocks and precious metals have found buyers.

This dramatic shift carries significant weight due to the evolving landscape of the market. Historically, Bitcoin's price was primarily determined by retail traders on offshore exchanges. However, over the past two years, the influx of capital into spot ETFs and the CME's emergence as the primary venue for futures trading have changed the dynamics. Institutional investors, including pension funds and hedge funds, have largely replaced individual buyers, making American retail and institutional capital the marginal price-setter. The market reached a record high of $67,500 on October 6, but it has since stalled without any clear catalyst to reignite its momentum.

The underlying issue seems straightforward: the institutional thesis behind Bitcoin has faltered. Investors who purchased Bitcoin as a hedge against inflation or economic instability have witnessed its decline alongside, and in some cases even more rapidly than, the risks it was intended to mitigate. Those who viewed it as a momentum play have shifted their investments towards more stable assets, such as gold and global stocks.

The unwinding of the crypto trade has resulted in a market that appears thinner than it might seem at first glance. David Lawant, head of research at Anchorage Digital, noted that demand for borrowed exposure on the CME has not been this muted since the pre-ETF run-up of mid-2023. The lack of leverage in the market means there are fewer forced buyers when prices rise and fewer natural absorbers when selling pressure increases.

Interestingly, a significant portion of the institutional investment surge was more mechanical than it appeared. Hedge funds employed basis trading strategies—buying spot Bitcoin while selling futures contracts at a premium to capture the spread. This approach did not require a directional view on price movements, but rather relied on the return exceeding opportunities elsewhere. For most of 2025, this strategy was profitable. However, as the spread between spot prices and Treasury yields compressed after October 10, the rationale for this trade diminished, leading to a halt in the flows.

“That capital has no reason to stay,” said Bohumil Vosalik, chief investment officer at 319 Capital. “Until genuine spot demand returns, every bounce risks becoming a sell-to-even zone rather than a foundation for recovery.”

The ongoing negative Coinbase premium suggests that demand has yet to materialize. Despite Bitcoin's integration with U.S. finance yielding benefits like improved liquidity and enhanced legitimacy, the market is now in retreat, struggling to respond to positive news. For example, when BlackRock Inc. announced a product linked to Uniswap, the token experienced a brief rally before quickly reverting back. In previous cycles, similar announcements often ignited extended upward runs; currently, enthusiasm seems to wane before it can build any momentum.

The structural problems at play are also notable. The institutionalization of Bitcoin did not eliminate its volatility; rather, it has merely redistributed it. The very products that brought Wall Street into Bitcoin—ETFs, yield-generating overlays, and options strategies—were designed to stabilize returns under calm conditions. However, these products can concentrate risk in ways that only become evident during market upheavals.

Structured products that generate yield by selling options can suppress price fluctuations during stable periods, but they often amplify them when significant catalysts emerge. Many ETF investors currently find themselves below their average cost basis, meaning any price bounces are likely to be sold as holders seek to break even, thus capping potential advances. Spencer Hallarn, global head of OTC trading at GSR, remarked, “The growing embrace of products like BlackRock’s IBIT is creating localized stabilization in Bitcoin when prices trade in a range. But when a real catalyst hits, those same structures can actually exaggerate the move.”

In summary, the market for Bitcoin has lost its ability to respond to positive news, creating a challenging environment for investors. The unexpected volatility is not just a temporary setback; it signals deeper structural issues that could take time to resolve. As it stands, without a resurgence in genuine demand, the future of Bitcoin as a stable investment remains uncertain.

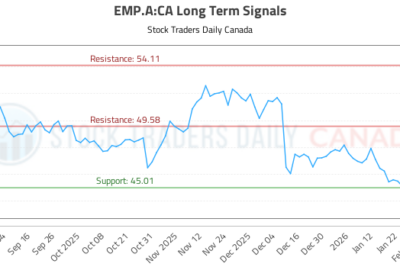

Why EMP.A Stock Just Plummeted 40%—Investors Are Panicking! Are You Next?

Shocking Resignation: Why This Health Clinic Director’s Sudden Exit Could Impact Your Care!

Nvidia's Shocking Software Reports: Will This Trigger a Stock Market Collapse? Find Out Now!

You Won't Believe Why This Shocking Legal Case Is Keeping Millions in the Dark!

Josh Stein's Shocking Revelation at White House Meeting: What You MUST Know About North Carolina's Future!

Statiq's Shocking $18 Million Funding: What This Means for Your EV Future!

You might also like: